Market News

Mortgage Rates Top 6.77%: What It Means for Home Buyers

Mortgage rates ticked back up this week after a brief pause, and if you are planning to buy a home, this is a good moment to understand what is driving the movement and how to think through your next steps clearly and calmly.

Where Rates Stand Right Now

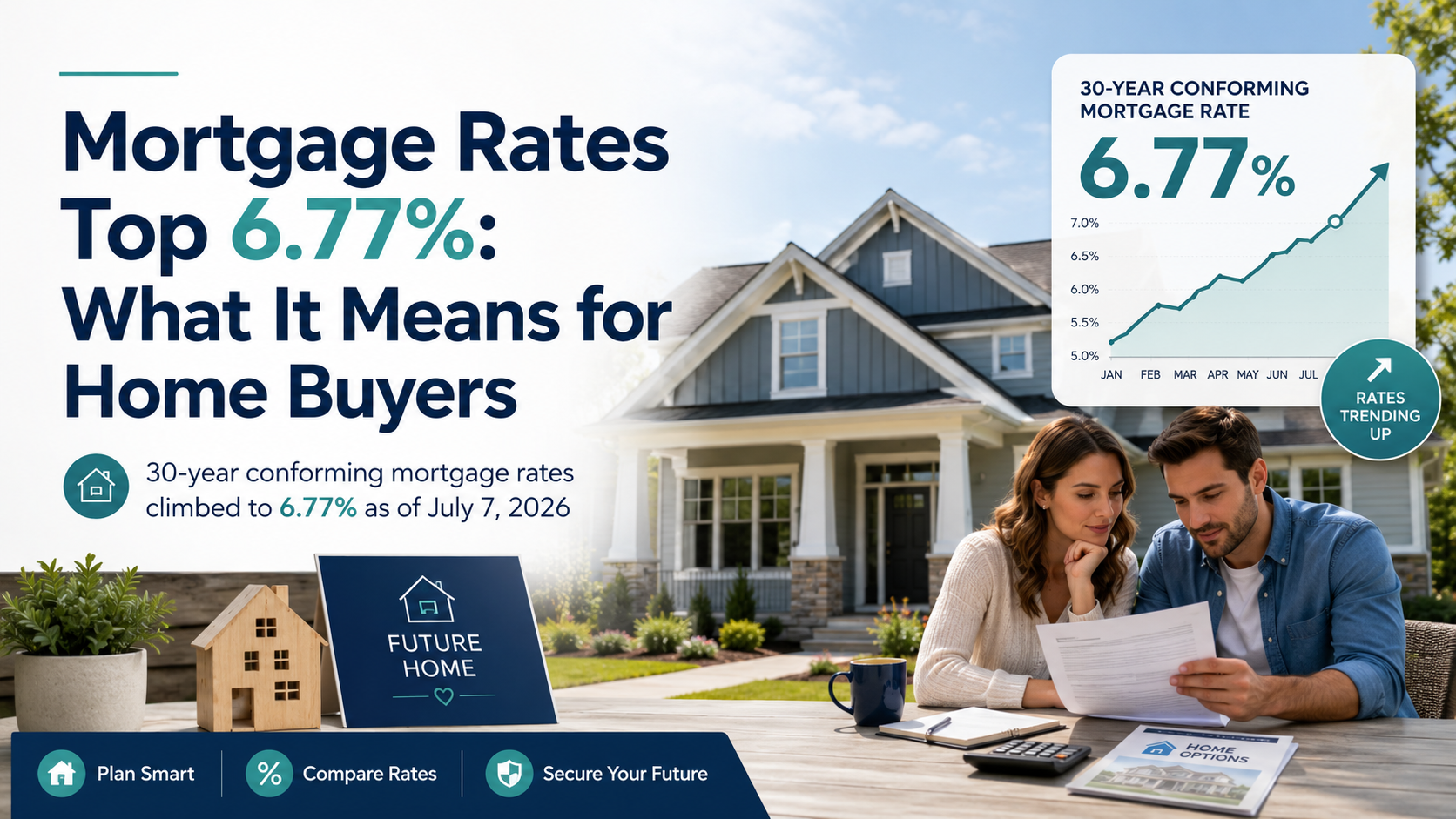

According to HousingWire's Mortgage Rates Center, as of July 7, 2026:

- 30-year conforming loans averaged 6.77%, up 4 basis points from the prior week

- 30-year jumbo loans averaged 6.75%, up 9 basis points

- 30-year FHA loans averaged 6.35%, up 6 basis points

For context, FHA loans remain noticeably lower than conventional conforming rates, which is worth keeping in mind if you are a first-time buyer with a smaller down payment or a lower credit score.

Why Rates Moved Higher Again

Last week offered a small reprieve, with rates dipping across the board. This week, that reversed. The main driver, according to HousingWire, is ongoing hawkish messaging from the Federal Reserve around inflation and monetary policy.

Adding fuel to the fire: the Federal Reserve Bank of New York released its June Survey of Consumer Expectations on July 7, drawing on responses from roughly 1,300 households. The survey found that median one-year inflation expectations rose to 3.7%. In plain terms, everyday Americans expect prices to keep climbing in the near term, and that kind of sentiment tends to keep upward pressure on borrowing costs, including mortgage rates.

When inflation expectations stay elevated, lenders price that risk into the rates they offer. The Fed's reluctance to signal near-term rate cuts reinforces that dynamic.

The Silver Lining: Market Conditions Are Improving

Here is something worth holding onto: the broader housing market picture is not all bad news for buyers right now.

Bob Broeksmit, president and CEO of the Mortgage Bankers Association, noted in commentary cited by HousingWire that last week's modest rate dip was enough to lift home purchase demand slightly, and that demand is currently running ahead of last year's pace. He also pointed to two encouraging trends:

- Inventory is growing. National active inventory has climbed to over 852,000 listings, a meaningful improvement from the severely constrained supply of recent years.

- Home price growth is moderating. Price appreciation is easing in many areas, which helps buyers who have been priced out or stretched thin.

More supply and slower price growth can offset some of the affordability pressure from higher rates, at least partially. If these trends continue through summer, they could create real opportunities for buyers who are financially prepared.

What This Means for Your Budget

A rate move of a few basis points may sound minor, but it compounds over a 30-year loan. Here is a rough illustration of how rate levels affect a monthly payment on a $350,000 loan (principal and interest only):

- At 6.50%: approximately $2,212/month

- At 6.77%: approximately $2,278/month

- At 7.00%: approximately $2,329/month

That is a difference of roughly $66 per month between 6.50% and 6.77%, or nearly $800 per year. Over the life of the loan, it adds up to real money. Knowing your actual numbers, based on your specific loan amount, down payment, and credit profile, is far more useful than any general estimate.

Ready to see how today's rates affect your real purchase budget? Head over to The Homebuyer Toolkit and start for free. You can run your numbers against current rates, explore down payment assistance programs in your state, and build a buying timeline that fits your situation.

What to Consider as a Buyer Right Now

A few practical thoughts if you are actively shopping or preparing to buy:

- Get pre-approved sooner rather than later. Locking a rate at the right moment requires being ready to act. Pre-approval puts you in that position.

- Look at FHA loans if you qualify. At 6.35% versus 6.77% for conventional loans, FHA financing could meaningfully improve your monthly affordability.

- Do not try to time the bottom. Rates have proven unpredictable week to week. If the home, the price, and the payment work for your budget today, that matters more than waiting for a rate that may or may not arrive.

- Factor in the full picture. More inventory and moderating prices are real positives. A slightly higher rate in a better-supplied market may still be a better deal than a lower rate in a frenzied, over-bid market.

The Bottom Line

Mortgage rates are at 6.77% for 30-year conforming loans as of early July 2026, pushed up by inflation concerns and a Federal Reserve that is in no hurry to cut. That is real affordability pressure, and it deserves honest attention. At the same time, inventory is growing and price growth is cooling, which creates a more balanced environment than buyers faced in recent years. The best move right now is to know your numbers, understand your options, and stay ready to act when the right opportunity comes.

Stop reading about buying a home. Start doing it.

- Run your real numbers against today's rates

- Find down payment assistance for your state

- Build a personalized timeline, with a personal AI guide

Frequently asked questions

What is the current 30-year mortgage rate as of July 2026?

As of July 7, 2026, 30-year conforming mortgage rates averaged 6.77%, according to HousingWire's Mortgage Rates Center. FHA-backed 30-year loans averaged a lower 6.35%, and 30-year jumbo loans averaged 6.75%.

Why did mortgage rates go up in July 2026?

Rates rose primarily because the Federal Reserve continued to signal a hawkish stance on inflation. Separately, a New York Federal Reserve survey found that consumers' one-year inflation expectations climbed to 3.7% in June, which also puts upward pressure on borrowing costs.

Should I wait for mortgage rates to drop before buying a home?

Timing the market is notoriously difficult. While rates may eventually ease, waiting is not always the right strategy. If the home price, your budget, and the monthly payment make sense today, buying sooner could make more sense than waiting, especially as inventory improves and price growth moderates in many areas.

Are FHA loans a better deal than conventional loans right now?

FHA loans are currently averaging about 0.42 percentage points less than 30-year conforming loans (6.35% vs 6.77% as of early July 2026). For eligible buyers, especially first-timers with smaller down payments or lower credit scores, FHA financing can meaningfully reduce monthly costs. A licensed mortgage professional can help you compare options for your specific situation.

Is the housing market getting better for buyers in 2026?

In some ways, yes. Active for-sale inventory has grown to over 852,000 listings nationally, and home price growth is moderating in many markets. The Mortgage Bankers Association noted that purchase demand is running ahead of last year's pace, suggesting buyers are finding more opportunity despite higher rates.